U.S. East Coast states have recently experienced significant setbacks in offshore wind development including project cancellations and delays in the last year that have put their clean energy goals at risk. Most of these setbacks have been caused by temporary issues that will improve over time such as cost escalations from higher interest rates and inflation as well as supply chain constraints and bottlenecks. Still, offshore wind fundamentals remain strong in the long-term, and states have considerable tools at their disposal to address these recent challenges head on.

Why Are States Staying the Course on Offshore Wind?

To fully decarbonize the electric grid by 2035 and achieve one of President Biden’s central climate commitments, the United States must rapidly accelerate the deployment of clean energy and transmission and double or triple its wind, solar, and storage capacity this decade. The buildout of offshore wind is a critical component of this capacity, and the Biden administration is pushing to achieve the deployment of 30 gigawatts (GW) of offshore wind in the United States by 2030. States are at the forefront of this effort.

Despite recent U.S. project cancellations and delays, the fundamentals of offshore wind energy remain strong. Offshore wind is a proven 30-year-old technology that produces renewable energy when and where most U.S. households need it. With nearly 80 percent of U.S. electricity demand coming from the coastal and Great Lakes states, offshore wind is a local energy resource for most Americans that cannot be outsourced and has the potential to create tens of thousands of jobs. U.S. offshore wind is a reliable and plentiful energy source that also tends to be strongest during peak demand hours, with the potential capacity to generate more than 4,200 GW of power, according to the National Renewable Energy Laboratory. In short, offshore wind is one of the most efficient and powerful sources of renewable energy that will help us tackle the climate crisis and achieve our federal and state clean energy goals.

Moreover, there have been some significant signs of progress in these recent headwinds. Since the enactment of the Inflation Reduction Act (IRA), the industry has seen close to $3 billion of investment according to the U.S. Department of Energy (DOE). Projects have reached new milestones of construction, installation, and power transmission to the grid. Off the coast of New York, the first utility-scale project in federal waters, South Fork Wind, began construction and delivering power to the grid in 2023. The first U.S. commercial-scale offshore wind farm, Vineyard Wind, which is located off the coast of Massachusetts, began delivering electricity to the grid in 2024 and will deliver 800 megawatts (MW) of power when completed.

As such, governors and state legislatures along the coasts have set their own ambitious targets for deployment and stayed the course during recent market interruptions. States recognize the critical importance of offshore wind to combating the climate crisis, as well as the economic development and job creation potential for their states. Without offshore wind energy, it will be very difficult, or even impossible, for coastal states to decarbonize their electric grids fully. State leadership has been essential in catalyzing this essential industry, and implementation at the state level is what will ultimately determine whether offshore wind scales at the pace that is urgently required.

{kind=link}

Four Actions States Should Take to Get Their Offshore Wind Targets Back on Track

1. Increase Market Certainty and Accountability Through Improved State Offshore Wind Procurement Approaches

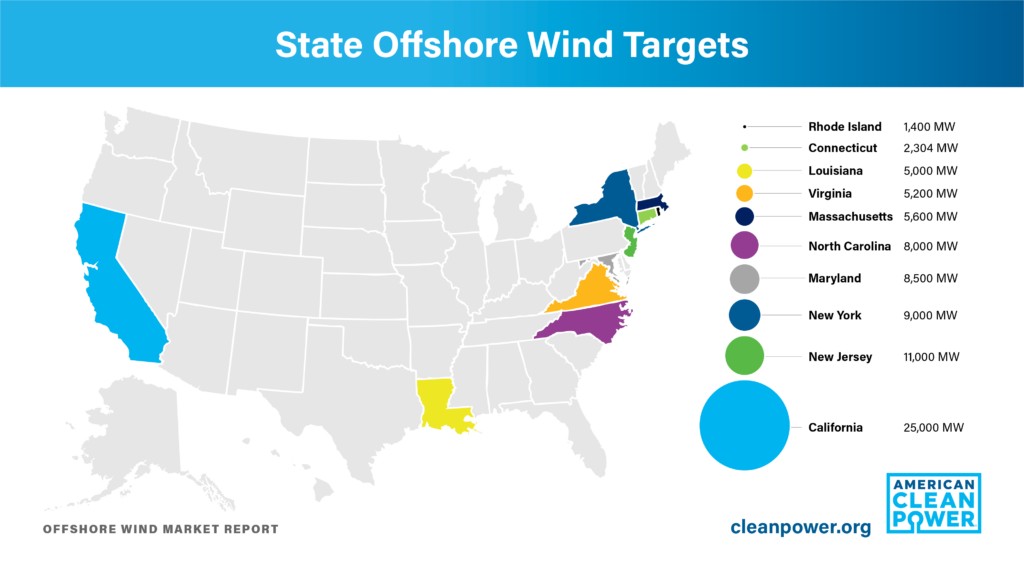

To help ensure future successful offshore wind development, offshore wind states should use recent market interruptions to reevaluate their procurement approach. First, states should set clear and achievable offshore wind targets and procurement schedules if they have not already. Most states have set overall targets, but most have not yet outlined a pathway or schedule to achieve these goals on time. Because states—rather than the federal government—procure offshore wind energy, the offshore wind industry needs to be able to plan and sequence projects and supply needs across multiple states and for multiple levels of government. This means there are more competing timelines that create more complex supply chain and sourcing logistics (e.g., vessel usage and steel procurement), in addition to the industry needing to recalibrate its planning after recent project delays and cancellations. Clear planning will help the industry and other key stakeholders identify and address supply chain bottlenecks and other potential cost increases before they become crises (e.g., vessel, steel, and cable shortages) and build a stronger business case for domestic supply chain investments. For example, New Jersey has set an offshore wind goal of 11GW with a clear and steady schedule to achieve its goal by 2040, including a revised accelerated procurement plan to account for recent project cancellations, and other states should follow suit.

Additionally, offshore wind-procuring states should conduct and regularly update offshore wind strategic plans to provide a clear north star for offshore wind developers and suppliers, policymakers, and other stakeholders involved in offshore wind procurements. An offshore wind strategic plan provides states with a roadmap for offshore wind development. It should include procurement timelines and goals, the state’s availability of and approach to infrastructure development such as transmission, vessels, and ports, expected state investments and market incentives, commitment to affordability and environmental stewardship, and approach to workforce development and collaboration. With the recent project cancellations and delays in U.S. offshore wind, states with plans must also update them to reflect how states are addressing these risks and close any gaps in their plans. Strong stakeholder engagement that involves the offshore wind industry, ratepayer advocates, community and Tribal organizations, and environmental and maritime stakeholders will be critical to the success of the strategic plan.

To complement a strategic plan, states should seek to administratively and/or legislatively update expected state investments and market incentives to reflect evolving industry and state needs as well as the increased value of federal tax credits from the IRA. State incentives should be revised to maximize the value of IRA tax credits (particularly bonus credits like the energy community bonus credit), meet the market where it is in terms of supply chain maturity, and promote sustainable local investments that can be potentially used as regional assets. Energy procuring and supporting agencies should also investigate how they can leverage programs recently available to states (as a result of the IRA and Infrastructure Investment and Jobs Act) to finance public offshore wind investments including direct pay (i.e., elective pay) and loans and loan guarantees (i.e., Title 17 loans) from the DOE Loan Programs Office. Qualifying state public or quasi-public institutions will need to be certified as State Energy Financing Institutions (SEFIs), if they are not already, to participate in Title 17 loan programs.

State energy procurements can also be strengthened to protect ratepayers from delays and cost increases as much as possible. One way states can do this is by including key performance indicators (KPIs) to ensure developer accountability in reaching critical development milestones. This will also help states identify and address potential development challenges sooner and promote greater project transparency. New York has incorporated KPIs in its most recently awarded solicitation that other states could adapt to fit their priorities.

Likewise, states can also better protect ratepayers from unanticipated or unavoidable cost increases such as federal permitting delays, inflation, and supply chain constraints—challenges that can arise for any type of energy source. Specifically, states can design more progressive rate structures so that the most energy-burdened families are not disproportionately affected. For example, one rate policy tool states can use is limiting utility bills costs based on income with percentage of income payment plans (PIPPs). States can establish PIPPs to directly limit energy bill costs for low-income households to an affordable rate such as no more than six percent of income. This type of tool should be paired with complementary efforts in energy efficiency and weatherization to maximize cost reductions. Several states including California, Connecticut, Colorado, Illinois, Maine, Nevada, New Jersey, New York, Ohio, Pennsylvania, and Virginia already have some version of a PIPP to alleviate energy burdens for low-income households but more comprehensive PIPPs are needed.

2. Invest in Port Infrastructure and Supply Chain Development

Port infrastructure and supply chain development have been major industry challenges globally. The demand for offshore wind has rapidly increased, inflationary pressures have temporarily increased the cost of production, and components have gotten larger and larger, creating challenges for existing and in-development facilities that need to be able to accommodate larger and heavier components. As states better understand the offshore wind market and address these temporary challenges, states should re-evaluate how they can best serve the offshore wind supply chain and seek to address major offshore wind bottlenecks like cables, towers, and vessels. This is an incredible opportunity for job creation and economic development, but states should seek to ensure that supply chain investments reflect evolving market needs. Likewise, port development is critical to localizing supply chains and jobs, and states should evaluate what types of port investments are appropriate for their offshore wind demand and investment capabilities (i.e., marshaling, manufacturing, and operations and maintenance ports).

States must plan to invest in and incentivize offshore wind supply chain localization if they are serious about creating long-term jobs and protecting against global supply chain constraints. New York provides a strong example of this in its most recent offshore wind solicitation, committing $500 million to support port, manufacturing, and supply chain infrastructure development and securing industry commitments for blade and nacelle manufacturing and assembly facilities. Likewise, New Jersey has committed $400 million to develop the New Jersey Wind Port, which will accommodate over 200 acres for offshore wind marshaling and manufacturing. While each state will have different abilities and appetites to invest in supply chain developments, there are more tools available than ever to support public investments in clean energy projects such as direct pay and Title 17 loan financing, as noted above. Regardless, states should be realistic about market demand and timing for localization. Investments should be made with a commitment toward sustainability to help ensure a factory or facility will continue operating long-term.

3. Commit to Real and Meaningful Regional Partnerships

While most countries take a national approach to offshore wind development, the United States’ state-by-state approach to development, layered on top of the complex federal permitting and review process, makes it more difficult to navigate and plan. Partnership is one of the most underutilized actions states can take to address this complex web and strengthen the offshore wind industry in their respective states and regions. From ports and supply chain development to procurement to even workforce development, states must find ways to partner together to maximize economies of scale and ensure economic benefits. Several states have taken initial steps to increase coordination: Massachusetts, Rhode Island, and Connecticut have recently signed an agreement to pursue a multi-state procurement; New York and New Jersey have developed a shared vision on supply development; and Maryland, North Carolina, and Virginia created a regional partnership.

Still, there must be more tangible commitments to fully realize the benefits of regional partnerships and enable industry to respond accordingly to these commitments. Meaningful partnership commitments could include but are certainly not limited to agreements to use joint assets such as ports, facilities, and vessels, coordination of workforce development and small business entry into offshore wind, development of joint procurements, and standardization of procurement practices. Partnerships with binding coordination commitments will help increase market certainty and enable offshore wind developers and suppliers to build stronger business cases for investment.

Another area ripe for increased partnership is community engagement. Not only do the multiple layers of siting and permitting at federal, state, and local levels create a broad and diverse set of stakeholders for community engagement and education, but offshore wind has also been combating coordinated misinformation campaigns funded by the fossil fuel industry. These campaigns have been spreading lies about offshore wind’s impacts on whales and marine mammals, birds, the fishing industry, tourism, and the environment. In fact, the evidence demonstrates that offshore wind tends to have a net positive or neutral impact on these groups and that climate crisis inaction is the real threat. Further, states have made robust commitments to ensure environmentally responsible development, participating in the Regional Wildlife Science Collaborative for Offshore Wind (RWSC), Responsible Offshore Science Alliance (ROSA), and the National Offshore Wind Research & Development Consortium (NOWRDC). Still, there remains a significant gap in coordinated regional community engagement to communicate the real benefits of offshore wind and prevent the spread of misinformation.

While many states have rightfully required developers to undertake robust stakeholder engagement, especially at points of interconnection or where there are potential viewshed impacts, developers cannot be the sole communicators of the benefits of offshore wind development. With several offshore wind projects recently canceled or in the process of renegotiation, developers may not be the most trusted messengers and states may need to rebuild trust in affected communities. States should use this industry reset period to coordinate their community engagement efforts better, establish and develop trusted messengers, and share resources to extinguish misinformation campaigns and bad-faith arguments. A regional offshore wind community engagement organization or entity through which states can share information and resources about community benefits and concerns would help states better communicate to communities and stakeholders the true impacts of offshore wind and stay ahead of misinformation campaigns.

4. Invest in Developing Workers for Offshore Wind and Renewable Energy Careers

Preparing workers for offshore wind and renewable energy career opportunities is one of the most important steps states can take to maximize economic benefit from offshore wind development. There are career opportunities at every phase of development, from siting and permitting to manufacturing, construction, and installation to operations and maintenance to decommissioning. Most offshore wind jobs are in manufacturing and construction, but there is a multi-year lead time between when projects are awarded and when manufacturing, construction, and installation begin. This means workforce development practitioners and unions have several years to prepare and train workers. Any training effort should include wraparound services to support equity and inclusion. Most of the occupations in offshore wind already exist and many are in high demand like welders and electricians, providing future offshore wind workers the option to work in multiple sectors. Massachusetts provides a strong example of workforce development through its multi-year workforce development investments at the Massachusetts Clean Energy Center.

U.S. offshore wind standards for workers and suppliers are still being established, and states, labor unions, and other workforce development practitioners are navigating the occupational and training needs for the industry. Many states have already conducted workforce analyses for offshore wind, and significant investments are needed to further realize these opportunities.

States can also invest in regional collaboration to help further demystify these opportunities and increase the economy and efficiency of offshore wind workforce development. Instead of taking a developer-by-developer or project-by-project approach, a cross-state approach would help ensure workers are trained for long-term careers and are empowered to work across projects and potentially related industries. In practice, this collaboration could entail sharing training materials, jointly funding programming, coordinating with unions and other workforce practitioners, and convening industry to standardize requirements.

The Federal Government Still Has a Critical Role to Play

While there are a number of steps states can take to stabilize their respective offshore wind developments, the federal government—particularly the U.S. Bureau of Ocean Energy Management and DOE—will still need to take steps to streamline the permitting process further and provide more market certainty for the industry. Likewise, states are unable to fully address key bottlenecks such as vessel development and transmission without federal leadership and financing support. States should continue to work with federal agencies to find solutions to these challenges in complement to the above state actions. Offshore wind is a critical piece of addressing the climate crisis, and we cannot further delay momentum.